13:43 PM, 6th January 2015, About 10 years ago

Text Size

Make 2015 the year that you no longer take known risks without first taking full consideration of the pros and cons, and by making sure that you’re implementing the appropriate upfront actions.![]()

In particular, as we move into a New Year, why would you choose to leave problems for your beneficiaries and families which can simply be mitigated by taking the correct steps by utilising the right strategies?

As a property investor, you are running a business and so, as in any business, there are inherent costs always built in, and protecting your assets should be viewed as simply that. Why jeopardise all of your hard work in building your wealth and resulting income streams both for now and the future?

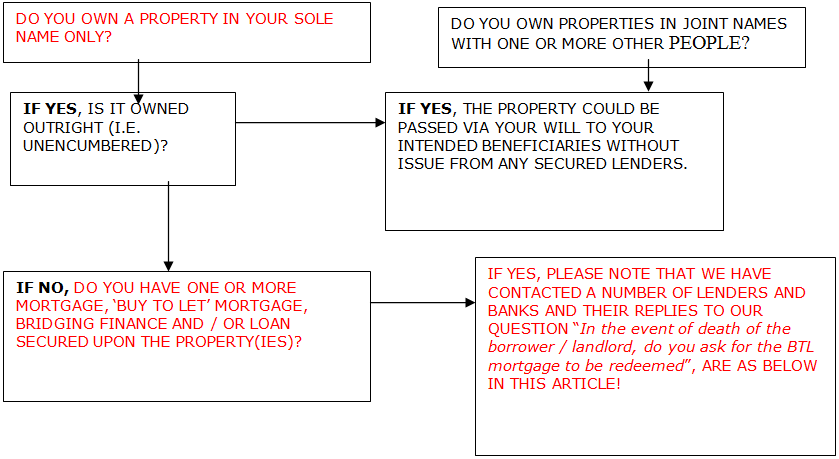

Lenders all have differing views and ways of dealing with the demise of a Mortgagor. Time is a luxury not often extended for very long.

As a serious reminder, we are able to outline our market research and findings below on such issues that occur all of the time. None of us are excluded from the possibility of this unforeseen scenario and circumstances.

Leeds Building Society

“We’d expect the mortgage debt to be repaid from either the cash funds held by the deceased’s estate or the sale of the property by the executor of the will.

Saffron Building Society

“In the case of the death of a sole borrower, then we are normally contacted by the executors who are dealing with Probate and the estate. In these circumstances, provided the mortgage payments continue to be met, we would normally allow a grace period of up to 12 months

Aldermore

“if sole borrower then technically we would require the account to be redeemed

The Mortgage Works

“I think it’s fair to say that whilst we would expect a sole mortgage to be redeemed; there would usually be a grace period permitted to allow for the estate to deal with matters.”

Principality Building Society

“In the event of a death of a borrower/landlord if the BTL mortgage was in a sole name we would ask for this mortgage to be redeemed in full.

So what can (should?) you do to protect your business, your assets and importantly, your family and beneficiaries?

Estate Planning & Trusts

Sound solutions should be sought and put in place;

1) a Basic Will being the prerequisite and further options considered for more complex estates.

2) Life Cover written under Trust to allow swift payment to Trustees on behalf of Beneficiaries. This removes the reliance on Probate being concluded, all that is simply required is the production of a Death Certificate.

Who Do You Know?

As a Financial Consultant I have been introduced to Clients in the last 12 months, who have developed a Critical Illness, lost members of their families – all of these incidents had no Critical Illness cover, no life protection whatsoever, yet with a substantial property portfolio now at risk.

The Beneficiaries are now dealing with a considerable bill for inheritance tax, with no provision or ability to pay in place. Those left behind are also having to deal with existing Tenants who have changed locks on properties, and of course they’re having to manage the biggest mistake of all – No Will!

I hope that if you are taking your time to read this you will be motivated to start 2015 with the crucial areas of business planning, life cover in Trust and implementing appropriate Wills and LPA’s, at the top of your “Action” list.

May we wish you all a Happy, Healthy and Prosperous New Year, with peace of mind that your affairs are properly in order.

Previous Article

Section 21 and Prescribed Information problemsNext Article

Is a log fire in a BTL madness??!