0:01 AM, 3rd January 2024, About A year ago

Text Size

The number of people buying their first home with a mortgage dropped to its lowest level in 10 years in 2023, as rising interest rates and inflation made it harder to afford a property.

According to Yorkshire Building Society, only 290,000 first-time buyers secured a mortgage last year, a 21% decrease from the previous year.

This is the lowest figure since 2013, when 260,000 first-time buyers entered the mortgage market.

A record proportion of borrowers opted for mortgages of more than 35 years to reduce their monthly payments and get on the property ladder.

Yorkshire’s director of mortgages, Ben Merritt, said: “First-time buyers are the lifeblood of the market and are still clearly keen to buy.

“The wider market relies on them, not least to support purchases higher up the chain.”

The research also shows that many potential buyers faced difficulties in saving for a deposit, as high inflation and record rent increases eroded their incomes.

They also had to pass stricter affordability checks by lenders, who raised the cost of an average fixed-rate mortgage from around 2% to 5% since the Bank of England started to hike interest rates in December 2021 to curb inflation.

The Bank has paused its rate rises in recent months, sparking some hope that mortgage rates could fall this year – but some analysts warn that rates could stay high for longer.

In contrast, more than 400,000 first-time buyers got a mortgage in 2021, benefiting from low borrowing costs and temporary stamp duty relief.

But that trend reversed in 2023, as living costs and interest rates increased.

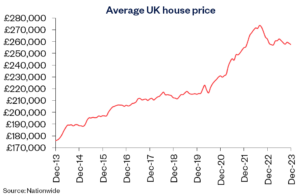

The new figures come shortly after Nationwide revealed how stretched housing affordability has become with a typical first-time buyer earning the average income and putting down a 20% deposit would have to spend 38% of their net income on their mortgage payment – well above the long-term average of 30%.

Meanwhile, first-time buyers accounted for more than a quarter (28%) of the housing market in 2023, the Skipton Group, which includes Skipton Building Society and Hamptons Estate Agents, says.

This is a steady rise from 16% in 2015, despite challenging economic conditions, including the recent pandemic and market fluctuations.

Aneisha Beveridge, head of research at Hamptons, said: “First-time buyers who have been able to successfully navigate 2023’s higher interest rates have increasingly found themselves at the front of the home-hunting queue.

“With nothing to sell in what’s been a tough market, those buying their first home are being favoured over offers from anyone with somewhere to sell, often even when their offer is a little lower.”